SOURCE: Center for American Progress

Download this testimony (pdf)

Read this testimony in your web browser

Thank you Chairman Baucus and Ranking Member Hatch for the opportunity to appear today to discuss the federal budget deficit.

The risks associated with the nation’s long-term deficit challenge have been well documented by numerous independent experts, including those at the Center for American Progress, so my testimony will not focus on that today. Suffice it to say that, while our immediate deficits are necessary and appropriate given the state of the economy, the projected long-term deficits that would result from maintaining current policies are unsustainable and highly problematic.

It has been encouraging that, for the last several months, the public debate over how to solve the long-term deficit problem has entered a new, much more sincere and substantive, stage. To a significant degree, we have moved beyond the mere posturing that had characterized the previous stage of debate when most were saying how much they deplored the deficits but were staying deliberately vague about what they’d do about them. Now, finally, we are starting to see the range of possible choices put before Congress and the public. This is a critical breakthrough. The posturing stage wasn’t just a problem because it delayed finding a solution; it was a problem because it perpetuated the pernicious myth that the problem could be solved without much pain. And as long as that myth survived, it meant great political risk to anyone who proposed a serious plan.

We at CAP like to take some credit for this breakthrough. We have been diligently outlining the difficulty of the challenges and offering specific solutions since 2009, and it’s been heartening to see the debate move to the point where we have a great deal of company.

Our most recent effort was to produce a long-term budget-balancing plan called “Budgeting for Growth and Prosperity,” which was released in May. In that proposal we offer a plan to balance the budget by 2030, 10 years sooner than the House-passed budget resolution. Our plan accomplishes this while still making important investments in the economy and strengthening the social safety net, and without damaging important middle-class programs or raising middle-class taxes on average. And, while our plan would raise taxes on the wealthy, the level is well within the range of historic norms. We also cut overall spending substantially relative to the CBO baseline. By 2035 our plan would lower spending by 4 percentage points of GDP compared to the baseline while revenue would be just half a percentage point of GDP above the baseline.

We cannot claim to have the only long-term budget plan in town. Many others have offered a wide range of plans to achieve fiscal sustainability. This just goes to show that the barriers to balancing the budget aren’t economic, they’re political. The United States is not like other countries that spend more than their economies can reasonably support and that face debts that they simply do not have the wealth to repay. Rather, our challenge is that we have simply decided not to pay for what we spend.

That’s not to say, of course, that the answer to our fiscal woes is simply to raise taxes to cover all of our spending. Note that if we were to do so we would still be one of the lowest-taxed countries in the world. We could do it without crippling ourselves economically. Nevertheless, I know of no one who is advocating such a solution. There is much work to do on the spending side as well. It is clear we need to contain health care cost growth, although there are huge differences in opinion as to how. And many of us believe that it is not sustainable to maintain defense spending at levels above the apex of the Cold War buildup under President Ronald Reagan, with the United States spending about as much as the rest of the world combined. And certainly a dedicated effort to wring efficiencies out of the day-to-day operations of the federal government could and should yield savings. It is for these reasons that our plan does not simply raise taxes to cover projected spending.

But just as the answer should not be a tax-increase-only plan, neither can the answer be a spending-cut-only plan. There are those who subscribe to the “It’s a spending problem not a tax problem” school of thought. But that’s a choice not a fact.

And the House of Representatives has given us a good insight into the consequences of that choice through their budget resolution. Their plan is designed to eventually balance the budget without allowing tax revenues to exceed 19 percent of gross domestic product. In order to accomplish that goal, the House budget makes enormous cuts to some very fundamental programs, dramatically constrains public investments that are key to future economic growth, and all but shreds the social safety net.

The most well known of these massive cuts is the House plan for Medicare. Under the House budget plan, Medicare, as it is currently structured, would cease to exist. In its place, retirees would receive a voucher, the value of which would rise much slower than the cost of health care. The ultimate effect is to shift thousands of dollars of costs onto each senior citizen. That might help bring federal spending down, but it does little to control health care inflation, and it certainly doesn’t help America’s seniors. In fact, we’ve estimated, based on the Congressional Budget Office’s analysis of the House budget, that the average senior will have to pay an additional $6,000 in insurance premiums. By 2030, that added cost will rise to $11,000.

But shifting health care costs from the federal books onto senior citizens is only one of the many onerous cuts proposed by the House budget. Their plan would also slash Medicaid down to the bone. Though many think of Medicaid as a program only for the very poor, in fact two-thirds of Medicaid dollars are spent on the elderly and the disabled. And fully 70 percent of nursing home residents benefit from Medicaid. Without Medicaid, the costs of caring for them would fall to their families, many of whom are middle class.

The House budget also makes draconian cuts to key areas of public investment, like education, transportation, and scientific research. In fact, the House budget would slash education funding by 53 percent, compared to current levels. Transportation and infrastructure would decline by 37 percent. And basic science and technology research and development would suffer a 28 percent cut, compared to today’s levels.

Suffice it to say, the American public did not react with very much warmth to the specifics of the House budget proposal. Given the magnitude of the cuts required to keep taxes so low, it’s hard to blame them.

But these are the kinds of cuts that are required if you want to keep tax revenue near the average level from a time gone by. You often hear that, over the past six decades, federal revenue has averaged 18 percent of gross domestic product. And while that is true, as far as it goes, it is not at all clear why future budgets should be constrained by past levels of revenue. In fact, because of demographic changes, the rising cost of health care, and emerging economic challenges, past levels of spending and revenue are essentially irrelevant. What might have worked in 1966—the last time federal spending matched 18 percent of GDP—will simply not work now, let alone 10 or 20 years from now.

Trying to shoehorn our future needs into past levels of revenue will necessarily result in damaging cuts to popular programs, benefits, services, and investments. And our view is that such an approach is not what’s best for the country. We believe that we’re better off having additional revenue in the mix. For one thing, tax revenue is very low. Currently, total federal revenue is at its lowest level since 1950 as a share of GDP. Yes, the weakness of the economy has much to do with that fact. But the interaction between the economic weakness and the low rates of the Bush tax regime together produced the historically low levels of revenue we are currently experiencing.

We also have low taxes relative to other economically developed countries. Only Mexico, Chile, Turkey, and South Korea had lower taxes as share of their economies from 2004 to 2008 among the 30 OECD countries. Just because our taxes are low doesn’t necessarily mean that they should be higher. But consider that if instead of ranking 26th out of 30, we were 19th, which would mean we collected the same amount of revenue as Canada as a share of our economy, then we would eliminate the budget deficit problem without facing draconian spending cuts like those in the House budget resolution. As an aside, it is worth noting that Canada is also in much better economic shape than we are right now.

While there is clearly room to raise more revenue overall, we believe, in particular, that there is room to raise taxes on the well off. Top marginal tax rates and capital gains tax rates are at historically low levels. Effective tax rates on the well off have plunged. And at the same time that these rates have been dropping, the incomes for the wealthy have been rising dramatically. Between 1979 and 2007 the richest 1 percent saw their before-tax incomes more than triple, adjusted for inflation. Just between 2001 and 2007 this same group’s before-tax income went up by over 50 percent. With declining taxes, their after-tax income went up even more.

The issue of whether or not to extend the Bush tax cuts for the well off has obviously been a matter of hot dispute. But we should put the potential impact on the wealthy in perspective. Consider that the effect on the top 1 percent would be an after-tax income decline of just 4.4 percent. If the income growth of the wealthy continues at the pace it has been rising over the last 25 years, averaging over 5 percent per year, then they’ll make up the amount lost to higher taxes in just 10 months and continue to get further and further ahead as time goes on. In other words, for the richest 1 percent, if the Bush tax cuts were to expire in January, by October they’d still be richer than they were the previous December even though they’d be paying slightly higher taxes. It’s the equivalent of a 10-month pay freeze. Given that the middle-class has suffered through a pay freeze lasting a decade and counting, it hardly seems like a great imposition to ask the wealthy to pay a bit more as part of achieving vitally needed deficit reduction.

We’ve actually done this before. In 1993 President Bill Clinton raised taxes on the wealthy. Nevertheless, over the next seven years, the income of the richest 1 percent almost doubled. In short, if we’re worried about America’s wealthy losing the will to seek profits by investing, starting businesses, and hiring people—it seems that bumping up top marginal tax rates a few points does little to dampen their quest for greater income or the attendant benefits that brings to the economy. In fact, when one looks at the relationship between top marginal tax rates and job growth you find that the country has actually enjoyed higher job growth during years with higher top tax rates.

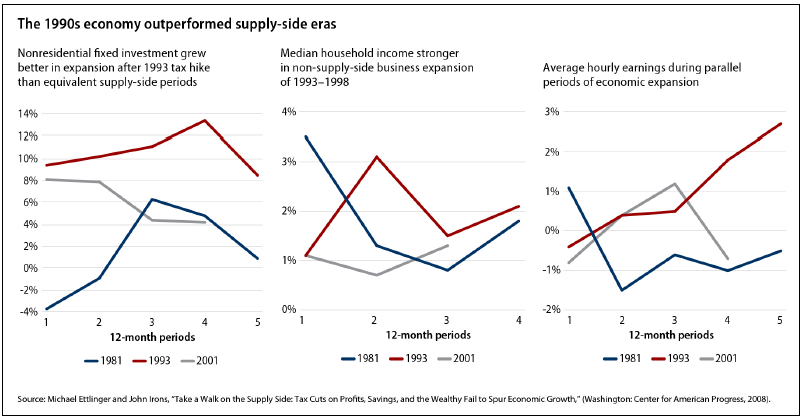

Of course, it wasn’t just the wealthy who did well under the Clinton-era tax code that we are scheduled to return to when the Bush tax cuts expire. The economy during 1990s grew at an historically high rate after taxes on the well off were raised under President Clinton. In fact, economic performance under the progressive tax policies of President Clinton far outstripped economic performance during the supply-side eras of Presidents Reagan and George W. Bush. Real investment, economic growth, median income, wage levels, and employment growth were all better in the Clinton era. And, of course, the federal budget boasted a surplus during the Clinton years in stark contrast to the experience under presidents Reagan and Bush.

It is telling that not only did the broad indicators of economic performance do better under progressive tax policies, but even the actual mechanisms that were supposed to be enhanced by supply-side tax policies worked better under President Clinton’s higher tax rates. Business investment and productivity in particular did better under President Clinton than under either President Reagan or President Bush.

The economic performance under President Bush’s tax regime has, of course, been particularly dismal. In the 2000s, even before the onset of the Great Recession, investment growth, job growth, and income growth were all lower than during any economic expansion in post-World War II U.S. history. The average employment growth over the period between the recessions of 2000-2001 and 2007-2009 was a mere 0.9 percent. This compares poorly to the average for postwar periods of economic expansion of 3 percent. Investment growth was 2.1 percent during the 2000s recovery compared to an average of 6.7 percent during past recoveries. And annual growth in our gross domestic product was 2.7 percent compared to an historic average of 4.8 percent.

And of course, during the Great Recession and its continuing aftermath we are still operating under the Bush tax regime. In fact, we’ve cut taxes even further. A third of the American Recovery and Reinvestment Act was tax cuts and last December the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010 also contained a substantial tax reduction. Lowering taxes as a way to boost economic growth, at least at the levels at which taxes are imposed by the United States, has proven to be disappointing as economic policy.

The reasons for the relatively weak economic performance during periods of substantial tax cuts for the well off compared to periods when taxes were higher may have nothing to do with tax policy. Other factors certainly influence the economy. To some degree, that is the point. Tax rates are not the be-all and end-all of economic growth. Other factors, including of course, what the government does with the taxes it collects, whether it makes important investments that help the economy, and myriad other private-sector trends and phenomena, are critical to economic growth. What is true, however, is that evidence that supply-side tax cuts help economic growth is weak at best and much contradicted in the economic literature.

Conclusion

Deficit reduction, as with anything that involves large scale spending and tax matters, is contentious. But it’s also necessary. Although at this moment it may seem like agreement is impossible, with the debt limit looming and no obvious path forward, in the end we will find a solution—because we have to. And the agreement will, in the long run, be determined by the American people. What’s been good about the last six months is that we’ve finally started having an honest conversation about these matters. People now know what a no-tax approach looks like. And they have a sense of the alternatives. In my view, we are going to end up with a balanced approach. The public will not stand for many of the spending cuts that have been put on the table. Nor are they anxious to see themselves taxed more heavily. And though we’re not there yet, there is a limit to how much the well off can be taxed without economic harm. There is a balancing to be done and what the American people want is a responsible balance. They don’t want a plan that is massively skewed one way or the other. That balance will not, however, be dictated by past levels of taxation and spending. After all, the country faces different needs now with an aging population and rising health care costs. With taxes at historic lows and spending needs on the rise it is evident to me which way the balance can and should move over the coming years. Delaying that movement will only result in a longer period of high deficits. And that would hurt us all.

Michael Ettlinger is the Vice President for Economic Policy at American Progress.

Download this testimony (pdf)

Read this testimony in your web browser